Donald Trump Heads to China as Sara Duterte Impeachment Vote Looms and SoftBank Reports Earnings

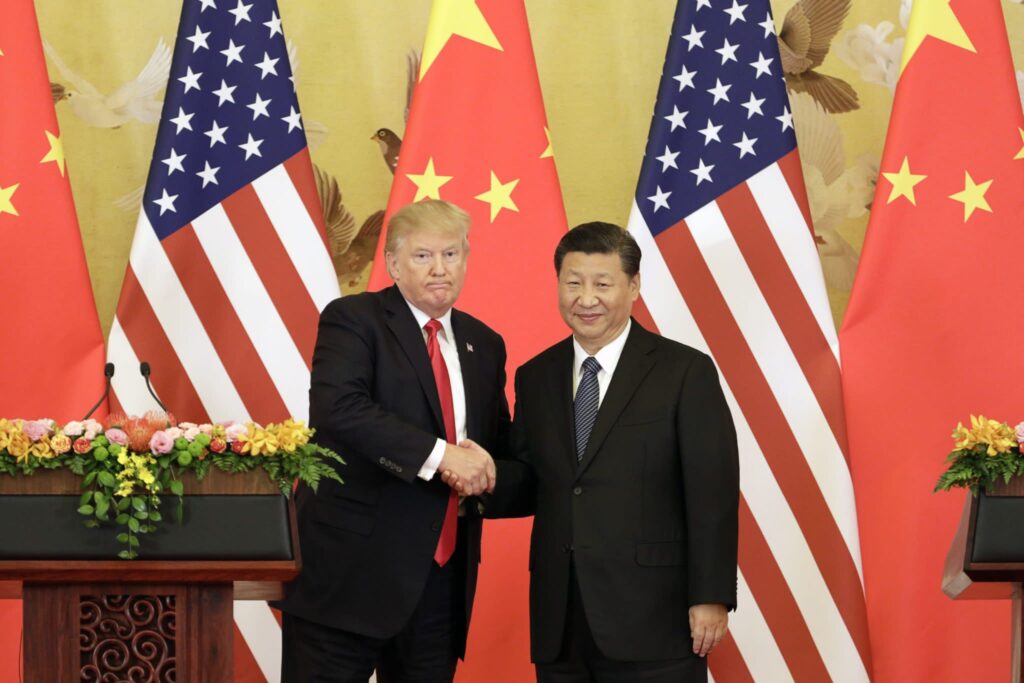

The global economic and political landscape continues to present a complex picture this week, with U.S. President Donald Trump’s anticipated visit to China standing as a central event. This high-level meeting, delayed for several weeks due to the U.S.-Israeli conflict with Iran, is expected to convene in Beijing, bringing together President Trump and Chinese President Xi Jinping. Discussions are likely to encompass strategies for maintaining their existing trade truce and navigating future investment and commercial ties, alongside more sensitive topics such as Taiwan. The American delegation accompanying President Trump is slated to include prominent figures from the technology and financial sectors.

Beyond the diplomatic movements, significant developments are unfolding across Asia. In the Philippines, Vice President Sara Duterte faces a critical parliamentary vote on her impeachment. The House of Representatives is poised to hold a plenary session to determine whether to proceed with impeachment. Should lawmakers vote in favor, the process would then advance to the Senate for further deliberation. This political event underscores the dynamic internal affairs within key regional nations.

Meanwhile, Thailand is preparing for the transfer of former Prime Minister Thaksin Shinawatra from prison to house arrest. This period of home detention is projected to last four months, with Shinawatra completing his full sentence in September. The move marks a notable shift in the legal proceedings surrounding the former leader, drawing attention to the country’s ongoing political narrative.

Financial markets are also keenly observing several major companies as they release their earnings reports. SoftBank Group is scheduled to announce its results for the fiscal year that concluded in March, with particular investor interest focused on its artificial intelligence strategy. The company’s investments in OpenAI are under scrutiny, especially given the rising competition from rival firm Anthropic, which has been steadily gaining market traction. This reflects a broader trend of investor focus on AI, a theme also evident in the upcoming earnings reports from Chinese and Taiwanese tech giants. Alibaba Group Holding is set to disclose its fourth-quarter results, while Tencent Holdings will report its first-quarter earnings. Additionally, Foxconn is slated to announce its first-quarter performance on Thursday, providing further insights into the technology sector’s health.

The economic implications of these events are far-reaching. U.S. Treasury Secretary Scott Bessent is undertaking a three-day visit to Japan, where he will meet with Prime Minister Sanae Takaichi, Finance Minister Satsuki Katayama, and Bank of Japan Governor Kazuo Ueda. Their agenda is expected to cover pressing issues such as currency fluctuations, strategies for energy procurement, and the wider economic impact of the Iran conflict. Following his engagements in Japan, Secretary Bessent will join President Trump’s delegation for the trip to China later in the week, highlighting the interconnectedness of these high-level discussions.

In the automotive industry, Japanese automaker Honda is preparing to release its financial results for the fiscal year ending in March. The company has publicly acknowledged facing significant losses, projecting a net loss of up to 690 billion yen ($4.4 billion) for the year, primarily attributed to strategic adjustments in its electric vehicle development. This would mark Honda’s first net loss since its listing in 1957. Reports have also indicated the automaker recorded its first operating loss in the recently concluded year. President and CEO Toshihiro Mibe is expected to outline the company’s future plans in light of these challenges.

Regional economies are also showing varied performance. Malaysia’s economy, for instance, is estimated to have experienced a slowdown in the first quarter of 2026. Advance figures suggest a year-on-year GDP growth rate of 5.3%, a decrease from the 6.3% recorded in the previous quarter. Despite this moderation, sectors such as services, manufacturing, and construction have maintained solid performance. Concurrently, the Malaysian ringgit has strengthened against the dollar, rising over 3.4% this year, even as market participants remain cautious regarding the potential effects of the ongoing conflict in Iran on energy markets and trade within Southeast Asia.

Related Posts

Sponsored Content